The sustainability-related double materiality assessment, introduced by the EU and relevant to also North American companies operating in the EU area, requires organizations to assess the impact of their activities on the environment and society. The GRI and ISSB’s IFRS standards serves the same purpose, only globally. Regardless of the reporting standard that an organization follows, gathering the relevant data and reporting it is a lot of work. We explain how Inclus’ collaborative tools help make the effort easier and more engaging to all stakeholders.

Introduction

One of the aims of the double materiality assessment is to engage all relevant stakeholders inside the organization and throughout its supply chain in assessing both the financial and impact materiality of their activities. Engaging relevant people is, in fact, an explicit requirement in the ESRS standard that drives the double materiality assessment efforts in organizations.

Yet it’s not just about adhering to regulative standards, EU’s or otherwise. Through engaging stakeholders with their insights, the double materiality analysis has the best chances of becoming granular enough to actually drive real strategic insights and impactful action points that may open up substantial new business opportunities.

What’s more, it’s not just the EU-regulated sustainability processes that benefit from Inclus’ tools and templates. The ISSB’s (International Sustainability Standards Board) IFRS S1 and IFRS S2 and GRI, the Global Reporting Initiative Standards, that drives the sustainability reporting and development efforts of many organizations in North America, can be equally supported with Inclus.

Double materiality is not only about communication; It is essentially a collaborative risk and opportunity management process

The double materiality assessment, demanded by EU’s Corporate Sustainability Reporting Directive (CSRD), is an evaluation process for organizations to determine the significance of sustainability-related topics. Double materiality assessment considers both the impact of these topics on the organization itself (the inside-out view) and how external sustainability developments can affect the organization (the outside-in view).

Double materiality analysis helps organizations identify and prioritize sustainability matters that are not only relevant to their operations but also crucial in addressing significant risks – and opportunities.

Process-wise, the efforts divide into phases that we will discuss in more detail in the rest or this article, coupled with illustrations of how these phases can be supported with Inclus:

Collecting data

Engaging stakeholders

Analysis

Reporting and Documentation

Action and Monitoring

Not the easiest of tasks

The amount of time and effort required from an average organization to conduct a proper double materiality analysis can vary widely depending on the organization’s size, complexity, industry, level of sustainability reporting maturity, and the availability of relevant data.

In terms of time consumption, conducting a comprehensive double materiality analysis can take anywhere from six months to a year or more, depending on the organization’s specific circumstances.

Note though that this is a continuous process, and organizations should regularly review and update their materiality assessments to ensure they remain relevant and aligned with evolving sustainability priorities and stakeholder expectations. The effort required can also vary from year to year as organizations become more experienced and efficient in conducting these assessments.

Regardless of the specifics, it is safe to say that conducting a double materiality analysis is a lot of work, as any ESG professional will be quick to confirm. Time and effort will be spent at least the following activities:

1. Collecting data

This stage can take several weeks to several months. It involves gathering data on both the internal and external aspects of sustainability, which may require collaboration across different departments and regions within the organization. The complexity of data collection can significantly impact both the timeline and the efforts required.

2. Engaging stakeholders

Engaging with stakeholders to gather their input and perspectives can take several months. This process includes identifying key stakeholders, conducting surveys or interviews, and analyzing the feedback received.

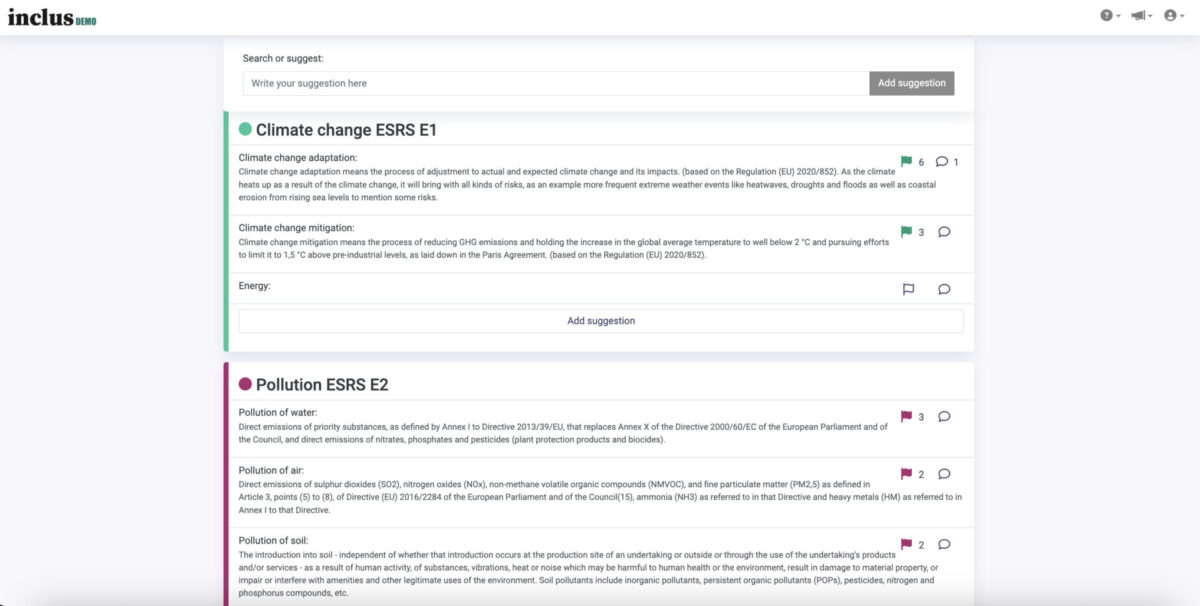

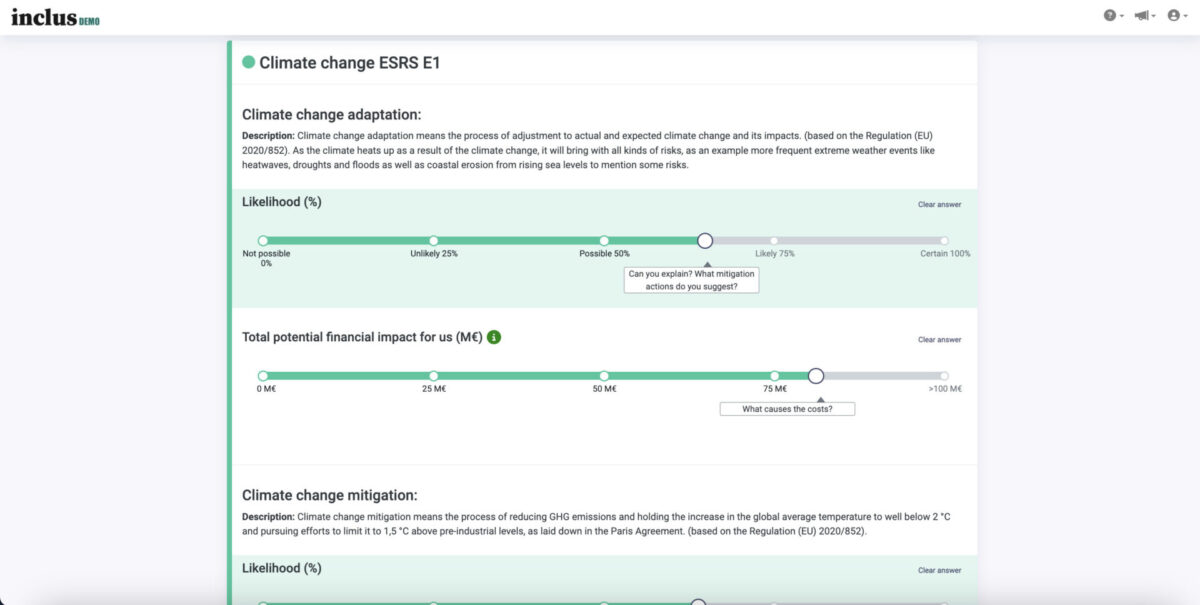

Inclus examples: Supporting Data collection and the Engagement of stakeholders

Inclus streamlines and optimizes the process through which participants share their materiality assessments for the themes that are included.

This approach actively involves stakeholders in a digital multi-criteria assessment, ensuring that a comprehensive array of perspectives is taken into account. This includes not only identifying potential risks but also recognizing valuable opportunities within the assessed themes.

By fostering collaboration and harnessing the power of digital tools, Inclus empowers organizations to make more informed decisions and create strategies that align with a broader spectrum of stakeholder viewpoints.

3. Analysis

Assessing the materiality of sustainability issues typically takes several weeks to a few months. This includes both quantitative analysis (e.g., using metrics and models) and qualitative analysis (e.g., considering stakeholder feedback and expert judgments).

Inclus example: Supporting Materiality Analysis through powerful visualizations

Inclus’ dynamic results visualizations are a powerful tool for analysis, providing valuable insights into materiality assessments.

These visualizations allow users to interact with data, uncovering trends and key themes with ease. They offer a comprehensive overview of the most important material themes, helping organizations focus on priorities and make informed decisions.

In essence, Inclus’ dynamic visualizations enhance analytical capabilities and guide strategic decision-making by distilling complex data into actionable insights. They empower organizations to align their strategies with stakeholder expectations and objectives.

4. Reporting and Documentation

Once the assessment is complete, organizations need to document their findings and integrate them into their sustainability reports. Again, this process typically takes several weeks.

Inclus example: Presenting Financial Materiality Overview

Inclus offers a highly adaptable approach to presenting a financial materiality overview in a digital report. Users have the flexibility to structure the report according to their specific needs, with a choice of predefined templates or custom layouts, catering to both high-level summaries and detailed analyses.

Visual elements, including charts, graphs, tables, and infographics, enhance the report’s visual appeal and facilitate the clear communication of complex financial data.

What sets Inclus apart is its interactive nature, featuring clickable charts and drill-down capabilities, enabling stakeholders to explore data deeply. Annotations provide context, and real-time data updates ensure the report remains current.

The flexibility, interactivity, and real-time capability make Inclus a powerful tool for crafting engaging and informative financial materiality overviews in digital reports, meeting diverse stakeholder needs and expectations.

5. Action and Monitoring

After the initial assessment, organizations should take action based on the findings. It is a good idea to go granular already in the data collection, stakeholder engagement, and analysis phases: To be able to draw genuinely meaningful insights that will help take equally meaningful and impactful action, one must usually dig deeper in the materiality assessment process than the topic headings level.

After its initial round, the double materiality assessment process becomes an ongoing one, and the organization should continuously monitor and update their analysis to stay aligned with changing internal and external factors.

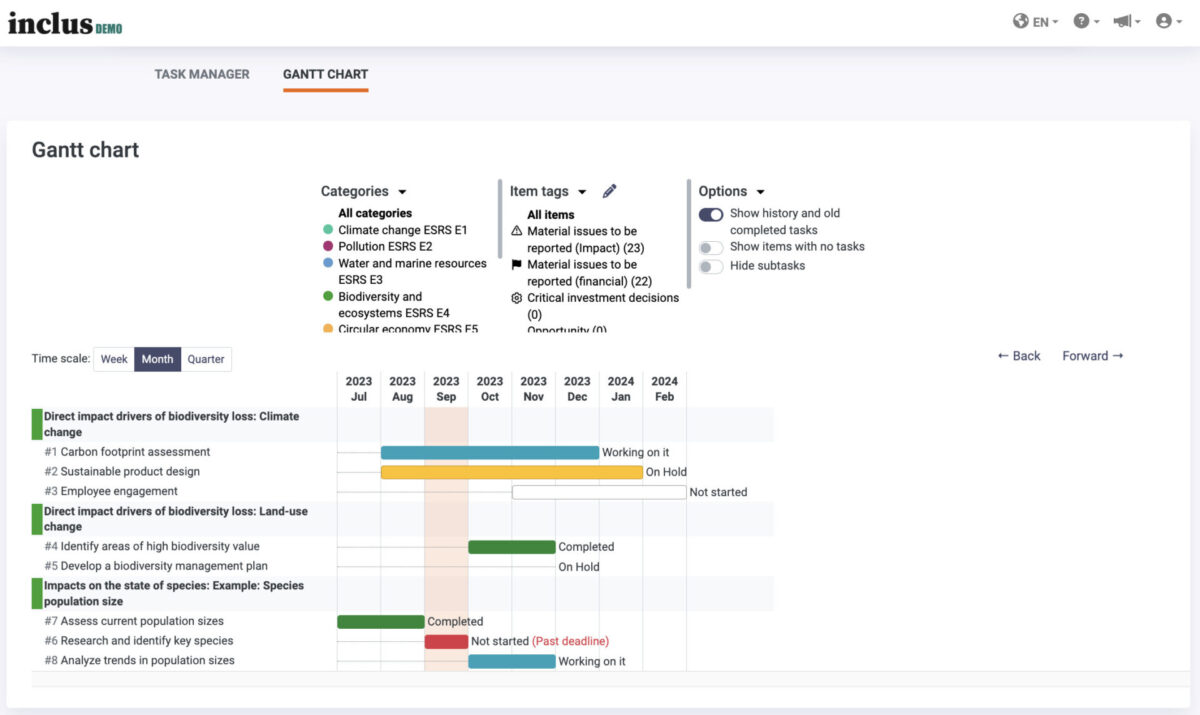

Inclus example: Supporting continuous Monitoring and Updates of Materiality analysis

Inclus’ task manager is a component that ensures materiality analysis leads to actionable results and continuous improvement. It streamlines the process by allowing organizations to track and manage materiality-related actions directly within the same system where the analysis takes place.

This integration eliminates the need to switch between tools, making it easier to turn insights into practical initiatives. It enables tasks to be assigned, deadlines set, and responsibilities allocated, ensuring that identified risks and opportunities are addressed effectively.

Inclus also promotes a recurring materiality assessment approach. This allows organizations to periodically revisit and update their materiality analysis, keeping it attuned to changes in the business environment, stakeholder priorities, and emerging risks or opportunities.

By regularly reassessing materiality, organizations can not only monitor the impact of their actions but also analyze how the materiality of different factors evolves over time.

In summary, conducting a double materiality assessment requires organizations to navigate data challenges, stakeholder engagement, and many times measurement difficulties, and the need to balance short-term and long-term objectives. These efforts and complexities underscore the importance of a robust and well-executed assessment process and tools.

Inclus helps organizations get started and up to speed with double materiality assessment easily and efficiently. With the ready-made and configurable double materiality template and process, Inclus smoothly streamlines data collection and helps engage the relevant stakeholders in different parts of the organization – or outside of it. Presenting the results of the assessment resented results is easy and powerful with visual and dynamic dashboards.

Want to know more? Let's book a demo

Related Sustainability content

- See our recent webinar recording where we go through the steps of double materiality assessment, supported by Inclus.

- See how TCFD (Task Force on Climate-related Financial Disclosures) and TNFD (The Taskforce on Nature-related Financial Disclosures) risk and opportunity analysis can be handled with Inclus software. Available here.

- Recap of recent panel discussion ”AI Assisted Digital Collaboration for a more Sustainable Future”. Available here.

- Recent blog: Navigating risk and opportunity with collaborative ESG processes. Available here.

‘Double Materiality’ in a nutshell

Conducting a double materiality assessment is not only a mandatory requirement outlined in EU’s Corporate Sustainability Reporting Directive (CSRD), but it also represents a significant opportunity for organizations to develop fresh sustainable business strategies and create value that may not have been evident before.

The crucial element here is the term ‘double’, which means that companies engaged in sustainability reporting must evaluate the significance of a sustainability issue from two distinct perspectives:

- Organizations must assess their impact on both people and the environment, representing the internal perspective (inside-out view). This involves considerations such as environmental harm or human rights violations.

- Secondly, organizations must examine how sustainability-related developments and events generate new risks and opportunities for the organization, reflecting the external perspective (outside-in view).

Within the framework of ‘double materiality’, a sustainability issue may hold material significance either due to its impact or from the perspective of risk and opportunity.

The CSRD does offer certain guidelines in this regard, yet the ultimate responsibility lies with the organization to assess whether a particular matter is material or not, and it must provide valid justifications for the decisions it makes.

Assessing which subjects are the most ‘material’ for an organization and, consequently, must be included in its sustainability reporting represents the first step in complying with the CSRD. The outcomes of this evaluation determine the content that should be incorporated into an organization’s sustainability reporting.